Guidance On Obtaining A Home Mortgage Straight From The Professionals

Created by-Wu SalomonsenWhen it comes to a home mortgage, the more you know, the better. The only way to be sure that you get the best deal available is to read up on all the information online. That will show you how to do it right, so start with the tips found below.

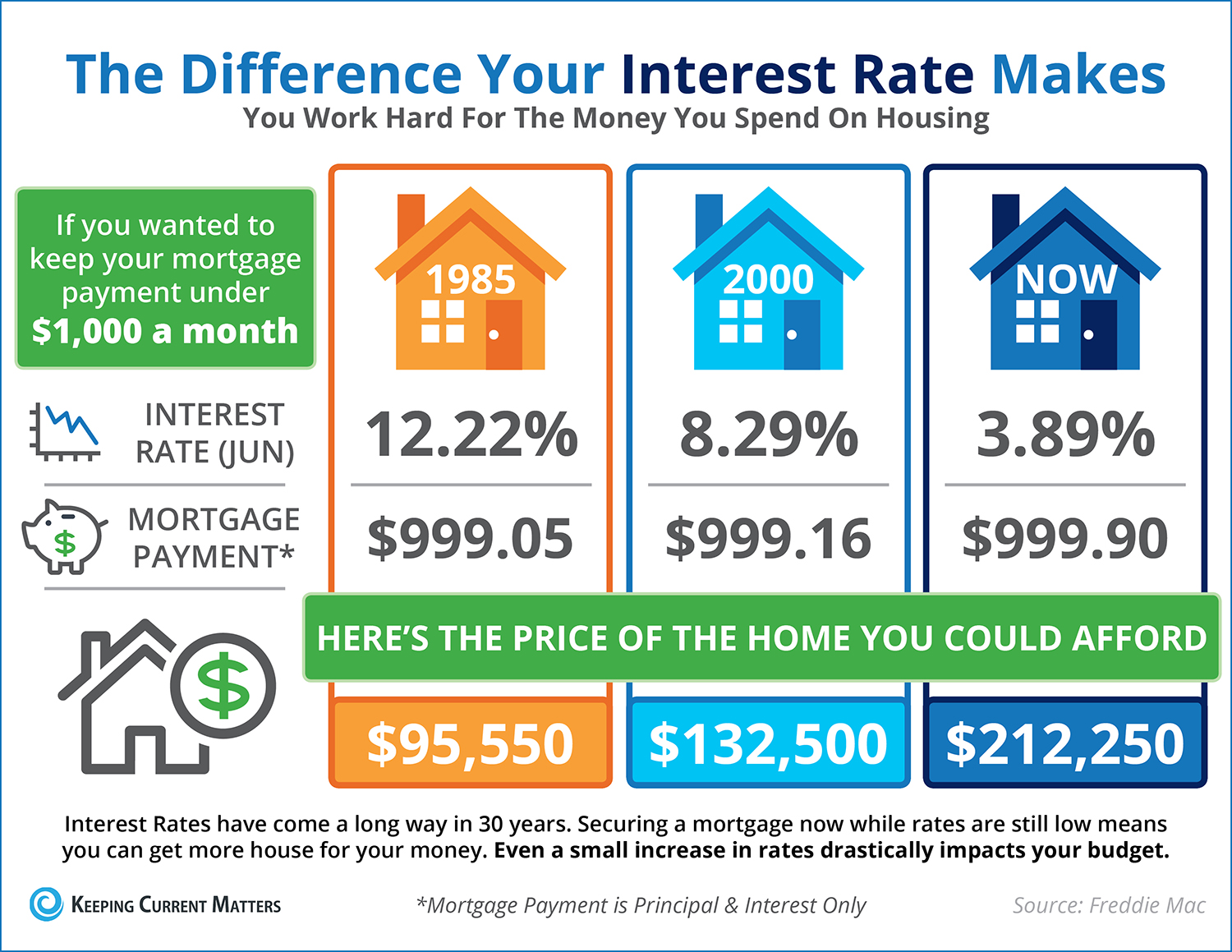

Before applying for a mortgage, pay down your debts. Lenders use a debt to income ratio to verify that you are able to afford a mortgage. A general rule of thumb is 36 percent of your gross income should be available to pay all of your monthly expenses, including your mortgage payment.

Before getting a mortgage, study your credit history. Good credit is what can help you get a mortgage. Obtain copies of your credit history and scores from the three major credit-reporting bureaus. Study your reports carefully to ensure that no issues or errors must be resolved before you apply. Many lenders need a minimum score of 680, which complies with Freddie Mac and Fannie Mae's guidelines. Most lenders want to avoid scores that are lower than 620.

Predefine your terms before applying for a mortgage, not just to show the lender that you can handle the arrangements, but to keep your monthly budget aligned as well. Buy a house that fits into your budget. No matter how much you love the home, if it makes you unable to keep up with your bills, you will wind up in trouble.

Some creditors neglect to notify credit reporting companies that you have paid off a delinquent balance. Since your credit score can prevent you from obtaining a home mortgage, make sure all the information on your report is accurate. You may be able to improve your score by updating the information on your report.

Get a copy of your credit score before you apply for a mortgage. It is best to know where you stand before you complete an application for a mortgage. You should check your credit even if you are sure you have a good score since identity theft or mistakes can occur.

Draw up a budget before applying for a home loan. It is important that you know how much you can realistically spend on a mortgage payment. If you aren't paying attention to your finances, it is easy to over-estimate how much you can afford to spend. Write down your income and expenses before applying for the mortgage.

Your loan can be denied by any changes in your financial situation. In order to obtain financing you must have a secure work history. If you're in the process of trying to get a loan, make sure you don't switch jobs before you're given one. Lenders will look to see how long you've been in your job position.

Don't apply for new credit and don't cancel existing credit cards in the six months before applying for a mortgage loan. Mortgage brokers are looking for consistency. Any time you apply for credit, it goes on your credit report. Avoid charging a large amount during that time and make every payment on time.

Do not sign a home mortgage contract before you have determined that there is no doubt that you will be able to afford the payments. Just because the bank approves you for a loan does not mean that you could really endure it financially. First do the math so that you know that you will be able to keep the home that you buy.

Understand the difference between a mortgage broker and a mortgage lender. There is an important distinction that you need to be aware of so you can make the best choice for your situation. A mortgage broker is a middle man, who helps you shop for loans from several different lenders. A mortgage lender is the direct source for a loan.

Try giving your lender a chance to help you with mortgage payment problems. If you struggle to make payments, do not ignore your lender's services. There are various new programs to help you keep up with your mortgage payments like forbearance if you have an FHA mortgage. https://www.nytimes.com/2021/10/11/business/ppp-loans-covid-racial-bias.html are generally happy to work out any delinquent loans via loan modifications, or possibly short sales if you can't afford to keep your home. It can be difficult to deal with them over this, but communication is key.

If you have a little bit more money to put down on a home, consider getting a conventional mortgage as opposed to an FHA mortgage. FHA mortgages have lower down payments, but excessive fees that are added to the cost of the mortgage. Save up at least 5 percent in order to be eligible for an FHA loan.

Boost your chances at of a lower mortgage rate by visiting your lender several months before submitting an application. Time is vital in the mortgage process.

Meeting with the lender months beforehand can help you fix issues like credit scores that could raise your rates. Usually when your offer is accepted, you will be quickly heading towards your closing date. This leaves little time to fix anything that could lower your rate.

Never assume that a mortgage is going to just get a home for you outright. Most lenders are going to require you to chip in a down payment. Depending on the lender, this can be anywhere from 5 percent to a full fifth of the total home value. Make sure you have this saved up.

Know the real estate agency or home builder you are dealing with. It is common for builders and agencies to have their own in-house financiers. Ask the about their lenders. Find out their available loan terms. This could open a new avenue of financing up for your new home mortgage.

Be sure to gather all your financial documentation and have it ready in a single file before applying for a home mortgage. You will need to have bank statements, tax returns, W2 forms and pay stubs on hand. Some lenders require additional documentation of income and responsibility. Be sure to find out what is needed before applying.

Most financial institutions want the assurance that the property they finance is insured and the property taxes are current. They do this by requiring that you add an amount to cover those expenses to your mortgage payments. This is called an escrow account, and most people find it is convenient to set up payments this way.

When the bank asks a question, be honest. It is a terrible idea to lie when applying for mortgage loans. Never misstate assets or income. If you do you could find yourself saddled with more debt than you can actually afford to pay. It may seem good in the moment, but in the long-run it will haunt you.

Now you know how to get a great loan without any headaches or stress. As long as you use the tips you've read here, you should have no problems in the future. Be sure to use this education so that you don't stumble over the hurdles the experts who wrote it have already dealt with.